Zimbabwe — Fractional Reserve Banking for USD is THE Problem

If you take USD1,000 cash and you go and deposit that at CBZ, they will credit your account with USD1,000 worth of electronic balances that you can use.

Because the bank now holds this deposit, it can lend say 80% of it to another person, who can either withdraw it as cash or get a credit entry to his account. This person now has USD800 available to spend.

The bank has created money. How?

- You still have USD1,000 to spend from your banking app.

- The person who borrowed from the bank now has USD800 to spend.

- In total there is now USD1,800 to spend.

- USD800 has been created out of thin air, by CBZ, in the form of lending.

- If the borrower comes to repay the USD800, the initial lending transaction is reversed. He doesn't owe the bank anymore, and the USD800 has been destroyed. We get back to having the original USD1,000 as the total money.

Money is thus being created via the lending process and destroyed via the repayment process. These processes of increasing and decreasing the money supply are perfectly-fine if the country is using its own currency. The problem comes when we increase and decrease the money supply for a currency that is not ours, a currency that we cannot print.

Dollars existing outside of the United States are called eurodollars. What we have in Zimbabwe is exactly that. Most countries, however, do not originate eurodollars (i.e. create new electronic balances). They do not allow their economic units to borrow and lend in USD unless the transaction is solely backed by dollars that come from the United States (either cash or USD balances held with banks in the USA). Countries that occasionally allow their banks to originate dollar loans within their banking systems tend to be large economies, with stable currencies (major currencies) and they typically have a Direct Swap Line with the Federal Reserve.

The Direct swap line allows the central bank of the country originating eurodollars to swap its own currency for USD. For example, the Canadian central bank gives Canadian dollars to the Federal Reserve in exchange for US dollars. The Federal Reserve bank holds those Canadian dollars for some time, and the Central Bank of Canada holds the US dollars for a time until the transaction is reversed. This transaction (the swap line) is typically referred to as a Liquidity Swap Line. The Fed has these dollar Liquidity Swap lines with 9 central banks.

What would happen if there were no swap lines?

The US dollars created outside of the USA would someday want to leave their countries of origination and flow into the global market. But the central bank of the particular country will not have enough balances with the Fed to allow such a clearing of those dollars. This is simply a matter of having created way too many USDs internally. This triggers a dollar-liquidity crisis within that country. At times, this crisis can spill into global markets, where there will be dollar shortages. These shortages simply mean foreign central banks do not have enough USD balances held at the Fed to facilitate their volumes of USD transactions.

Consider this scenario: let's say all central banks of countries other than the USA have a total of $3 trillion balances held with the Fed, yet the entities within all of these countries have USD balances worth $5 trillion. There will be a dollar shortage of $2 trillion. This shortage is a crisis.

You can ask, how come entities outside the USA can have $5 trillion worth of USD balances yet there is only $3 trillion known at the Fed? This is because the other $2 trillion worth of USDs were not created within the USA. They were created outside of the USA, without the knowledge of the Fed. They will be destroyed when loans that created these dollars are repaid (extinguished). Oftentimes, eurodollar loans to corporates and individuals are not long-term in nature. For governments, they can at times be of a longer-term.

In order to stabilize the global financial system, the Federal Reserve has to create more USDs and give these balances to the central banks of the other countries. You can think of this as the Fed creating the extra $2 trillion needed to back up those balances that were created outside of the USA. If they don't create these needed dollars, the liquidity crisis morphs into an international trade settlement crisis, since countries are so interconnected and dollar funding markets outside of the USA are an integral cog in the global financial system.

These newly created Fed dollars are given to other central banks in exchange for the currencies of those central banks. The transaction is established with a built-in reversal date. Why so, because the dollars created outside of the USA will have to be destroyed (via repayment) at some point in time.

The reality, however, is that dollar funding markets outside of the USA have continued to grow, and the Eurodollar market has exploded, hence the need for increasingly more swap lines, with longer durations.

Because the Reserve Bank of Zimbabwe has no liquidity swap line with the Federal Reserve, a dollar liquidity crisis inside Zimbabwe cannot be eased. RBZ cannot swap ZWL for USD with the Fed with a predetermined transaction reversal date.

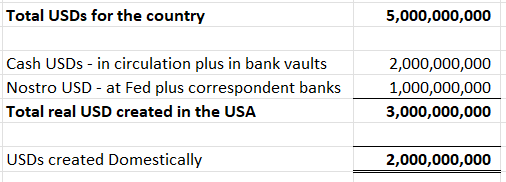

This absence of a backstop means all USDs created domestically have to fight with each other for being “backed” by the USDs created in the USA. The US dollars created in the USA exist in two forms: cash USD and real Nostro USD. The latter here means balances of USDs belonging to Zimbabwean banks but are held by banks outside of Zim, which links back to the Federal Reserve.

Because we are creating USDs domestically, you will not be surprised to find out that we can have $5 bn worth of USDs in the country, yet as a country, we only have $3 bn worth of USDs that were created in the USA. This $3 billion might exists as cash USD of $2 bn circulating in the economy and real Nostro USD of $1 bn worth of balances held with banks outside of Zimbabwe.

The $2bn worth of US dollars created domestically is the problem child. Why is it a problem? Because it also wants to go out of the country via imports. A person holding a domestically created USD electronic balance wants to make a telegraphic transfer (TT) to Japan to buy a car. Japan wants the settlement to go via the Fed network of banks so that they get a dollar that originated from the USA.

The Discount hits the Electronic Dollars

Because RBZ does not have a swap line that acts as a backstop, something has to give. Over time, the domestically created USDs can overwhelm the system as they can become larger than the real USDs created in the USA. The something that gives is the electronic USD balances in the Zimbabwean banking system. These USDs rightfully take the hit. After all, the local USDs are created by the banking system.

The electronic USD balances will be valued less than a cash USD, and less than real Nostro USD. This discount continues to grow, as long as the banking system continues to create USDs locally. The discount shrinks if the banking system destroys more local USDs than it creates.

Over time, everybody realizes that the local electronic USDs are not real USDs. At the end of the day, these internally created USDs end up not being USDs at all, but a proxy of our own currency given a nickname of the USD. The faster the real USD liquidity crisis hits, the more the need to create local USDs, and the more local USDs we create, the higher the discount to the real one. This happens over and over again until we get to that moment in time when we need to separate the goats from the sheep.

The Problem

The crux of the matter here is simple. It is the creation of USDs by the banking system when the central bank does not have a direct liquidity swap line with the Fed. The locally created USDs dilute the US-created USDs leading to the need for an eventual clean-up event.

When we create local USD, for local use, we increase the supply of local USD for transactional purposes, which disincentivizes economic units from using the local currency, driving down demand for the local currency.

Though the increased supply of USD via locally created dollars somewhat alleviates the shortage for transactional USD locally, the benefit comes at a huge cost to the system, which eventually has to be reset at some point.

The Solution

The solution is also simple. Banks should not be allowed to create USD dollars domestically. This means banks should have a 100% reserve ratio for USDs. Banks should not lend USDs that they do not have. Money creation should only be possible for the local currency.

The Futility of Dollarization coupled with Fractional Reserve Banking

The call for dollarization has been loud and clear. The plan is to solely use the USD as the currency.

The problem with this call is that it does not specify that we need to stop creating USDs locally. Simply dollarizing is not a full measure. It is a half-baked measure.

What's the point of dollarizing if our banks can create electronic USD balances from thin air? This is why the reserve ratio for USDs must be 100%.

If the reserve ratio for USD is 100%, banks cannot create USD balances from thin air. They can only lend what they have.

Dollarization coupled with Fractional Reserve banking is a futile exercise. We simply create more USDs than necessary. In other words, we end up with the very same situation we had last time, when we had so many USD balances in the banking system, and everyone agreed that the real USDs were long gone.

The person in the street will say RBZ, the government, and banks stole their real USD and gave them fake USD. If you ask them to prove it, they cannot prove that claim. How exactly does that happen? The irony is that the person making such a claim might have borrowed US dollars from a bank participating in the fractional reserve banking system, which is precisely the problem. So, “the thief” will be pointing fingers at others.

When the quantity of locally created USDs starts to overwhelm the system, economic units reduce the amount of cash that they deposit into the banking system. Exporters find ways of not bringing their forex receipts into contact with our banking system. The banking system becomes contaminated with “fake” US dollars. Any rational person tries to avoid exchanging a real Nostro USD for a USD that resides in our banking system, the same goes for cash USD.

Dollarization does not fix anything as long as it is equally yoked with the unbeliever (fractional reserve banking).

The Severe Austerity of Dollarization without Fractional Reserve Banking

Dollarization without fractional reserve banking is simply running the economy on a cash basis. It is severe. It is austere. It inhibits growth.

How do you run an economy without credit expansion? The severe austerity will lead to very little growth and a series of cash crises experienced by economic units. Banks cannot lend beyond their reserves, meaning they can only lend what they have, meaning no credit expansion at all. Credit will remain below the true levels of real USD. The money supply will not expand to facilitate economic activity.

The government will not be able to borrow domestically to cover budget deficits and temporarily in order to align cashflows. Corporates will reduce credit terms allowed for customers, preferring cash, since they cannot easily obtain working capital facilities from the banks. Banks will not be able to support the economy that much.

Without credit, both government and business will be occasionally crippled.

Under dollarization without fractional reserve banking, each electronic dollar in the banking system will be mirrored by either a dollar of cash in the bank’s vault or a dollar of balances that the bank holds outside of Zimbabwe.

If you go to CBZ and deposit USD1000, CBZ will take this money and lock it in their vault and give you an electronic balance. The electronic balance they give you is the only one they create. They don't create an additional USD800. Your electronic balance of USD1000 is 100% backed by cash in the bank’s vault.

If an exporter sells products for $1m, CBZ will get $1m credited to their account with Stanchart New York, and they give you $1m electronic balances to spend locally. The exporter’s $1m is 100% backed by a real Nostro balance.

This is all good. However,

- the economy suffers from not having enough USDs for transactional purposes.

- the economy suffers from not having access to US dollar credit (i.e., dollar funding markets).

- the economy cannot import more than it exports (forced to avoid a trade deficit) which typically results in shortages of key imports (fuel, medicines, etc).

When the liquidity crisis (not having enough USD) hits, it starts with the need for small change. Everywhere people will be scurrying for USD, and they just cannot find enough. The reason is simple, we can never ever have enough USDs to fulfill all our economy’s needs, as long as we are not yet a highly productive country. These needs are specifically:

- Transactional needs

- Savings needs

- Import needs

We get dollars from our exports, and these can barely cover the “import” needs, let alone the savings and transactional needs. You see, even with ever-growing exports, we can never ever have enough USDs.

At the end of the day, the government starts borrowing using O/D facilities at their CBZ Treasury Account in order to pay salaries, anticipating the next month’s receipts to fill up the O/D. The borrowing eventually morphs into Treasury Bills. Corporates follow suit until we are eventually back to fractional reserve banking.

In the real economy and the streets, deflation kicks in as people scurry around for dollar liquidity. Prices in USD start going down, driving down business margins. Some end up selling stock below ordering costs, just to get that much-needed liquidity. Eventually, they go out of business. People literally start begging for the authorities (government and central bank) to do something. The something that they beg for is the solution that becomes the next problem. We go back to square one.

So, What should we do?

Dollarization without fractional reserve banking is a severe austerity.

Dollarization with fractional reserve banking is a Mazoe Dilution Scam, which comes back to bite us at a certain point in time.

There is a cost to purchasing stability. We have to pay the cost.

What if we could index to a currency that is not as hard as the USD? What if we could index to a currency issued by a central bank that can allow us to direct swap line with them.

The cost of using the US dollar is high for our economy which does not have strong fundamentals.

If we are to have a dual-currency regime, which we have now, then we need to ensure that there is no fractional reserve banking for the USD dollar.

If we are going to solely use a currency other than our own, then we need to adopt a currency that allows us to have a swap line. Not a single Central Bank in the world will be crazy enough to open a swap line with RBZ.

The practical option, for now, is the dual-currency of USD and ZWL, coupled with no fractional reserve banking for USD. Liquidity needs can be accommodated via the ZWL fractional reserve banking.

Take note that the damage is already done. USD fractional reserve banking has already diluted USDs in that Mazoe dilution style.

The mess can be sorted.

Ciao!